UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 10-K

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the fiscal year ended December 31, 2007 |

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE EXCHANGE ACT OF 1934 |

| For the transition period from to |

COLUMBIA SPORTSWEAR COMPANY

(Exact name of registrant as specified in its charter)

| Oregon | 93-0498284 | |

| (State or other jurisdiction of incorporation or organization) |

(IRS Employer Identification Number) | |

| 14375 NW Science Park Drive Portland, Oregon | 97229 | |

| (Address of principal executive offices) | (Zip Code) | |

(503) 985-4000

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class |

Name of each exchange on which registered | |

| Common Stock | The NASDAQ Stock Market LLC |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer x | Accelerated filer ¨ | |||

| Non-accelerated filer ¨ (Do not check if a smaller reporting company) | Smaller reporting company ¨ | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

The aggregate market value of the voting common stock held by non-affiliates of the registrant as of June 29, 2007, the last business day of the registrant’s most recently completed second fiscal quarter, was $937,099,000 based on the last reported sale price of the Company’s Common Stock as reported by the NASDAQ Global Select Market System on that day.

The number of shares of Common Stock outstanding on February 15, 2008 was 35,106,391.

Part III is incorporated by reference from the registrant’s proxy statement for its 2008 annual meeting of shareholders to be filed with the Commission within 120 days of December 31, 2007.

DECEMBER 31, 2007

TABLE OF CONTENTS

PART I

| Item 1. | BUSINESS |

General

Founded in 1938 in Portland, Oregon, as a small, family-owned, regional hat distributor and incorporated in 1961, Columbia Sportswear Company has grown to become a global leader in the design, sourcing, marketing and distribution of active outdoor apparel, footwear and related accessories and equipment. Unless the context indicates otherwise, the terms “we”, “us”, “our”, “the Company” and “Columbia” refer to Columbia Sportswear Company and its consolidated subsidiaries. Over the past seven years, we have expanded beyond our flagship Columbia Sportswear® brand by acquiring and developing a portfolio of outdoor apparel, footwear, accessories and equipment brands, including Sorel®, Mountain Hardwear®, Montrail®, and Pacific Trail®. Each of our brands addresses the outdoor performance needs of specific consumer groups and is distributed through a targeted mix of distribution channels. As one of the largest outerwear companies in the world, our products have earned an international reputation for quality, performance, durability, functionality, dependability and value. We employ various marketing strategies to increase and reinforce consumer awareness of each of our brands. We have sought to leverage our brand equity by expanding directly and through licensees into related outdoor and lifestyle merchandise categories, promoting a “head-to-toe” outfitting concept. We believe these strategies will help us achieve our vision of becoming the dominant global leader delivering best-in-class, authentic, innovative brands that reflect a passion for the outdoors. In 2007, we distributed our products to approximately 14,000 retailers in over 90 countries.

Our business is subject to many risks and uncertainties that may have a material adverse effect on our financial condition, results of operations and stock price. Some of these risks and uncertainties are described below under Item 1A, Risk Factors.

Products

We group our merchandise into four principal categories—(1) outerwear, (2) sportswear, (3) footwear, and (4) related accessories and equipment. The durability, functionality and affordability of our products make them ideal for use in a wide range of outdoor activities, including skiing, snowboarding, hunting, fishing, hiking, backpacking, mountaineering and rock climbing, as well as for casual wear. We are committed to creating innovative and functional products. We use durable, high-quality materials and construction across all of our product lines. We believe our broad range of competitively-priced merchandise offers consumers one of the best price-value equations in the outdoor apparel, footwear, accessories and equipment industries.

Our portfolio of brands enables us to provide products for a wide range of consumers, including elite mountain climbers who use Mountain Hardwear gear, top endurance trail runners who wear Montrail shoes, cold weather enthusiasts who wear Sorel cold weather boots, entire families who wear Columbia and Pacific Trail outerwear, and individuals who wear Columbia sportswear and footwear for a variety of active outdoor and lifestyle pursuits.

The following table presents the net sales and approximate percentages of net sales attributable to each of our principal product categories for each of the last three years ended December 31 (dollars in millions):

| 2007 | 2006 | 2005 | ||||||||||||||||

| Net Sales | % of Sales | Net Sales | % of Sales | Net Sales | % of Sales | |||||||||||||

| Outerwear |

$ | 497.6 | 36.7 | % | $ | 496.5 | 38.6 | % | $ | 440.0 | 38.1 | % | ||||||

| Sportswear |

565.6 | 41.7 | 509.1 | 39.5 | 450.3 | 39.0 | ||||||||||||

| Footwear |

227.4 | 16.8 | 219.7 | 17.1 | 211.2 | 18.3 | ||||||||||||

| Accessories and equipment |

65.4 | 4.8 | 62.4 | 4.8 | 54.3 | 4.6 | ||||||||||||

| Total |

$ | 1,356.0 | 100.0 | % | $ | 1,287.7 | 100.0 | % | $ | 1,155.8 | 100.0 | % | ||||||

2

Outerwear

Outerwear is our most established product category. We currently develop and distribute outerwear products under our Columbia, Convert, Mountain Hardwear, Sorel and Pacific Trail brands. Our outerwear is designed to protect the wearer from inclement weather in everyday use and in outdoor activities, such as skiing, snowboarding, hiking, hunting and fishing.

Many of our jackets incorporate our popular Columbia Interchange System®, which features a 3- or 4-jackets-in-1 design. Jackets incorporating the Interchange System typically combine a durable, nylon outershell with a removable liner. The outershell and the liner may be worn separately or together. This layering approach provides the wearer with a jacket for all seasons and weather conditions at a reasonable price.

Columbia-branded hunting and fishing products constitute one of our most established product lines in the outerwear category. This line includes apparel for the serious hunter and fisherman. Our parkas, shells, vests, liners, bib pants and rain suits in this product line incorporate a variety of purpose-specific features that have made us a leader in this category of outerwear.

We also produce a separate line of Columbia-branded youth outerwear products. The market for youth outerwear is significant and we are able to use our expertise in outerwear design and sourcing to meet the needs of the youth market.

Our Convert® brand offers functional apparel products designed for snowboarding.

Our Mountain Hardwear brand consists of technically advanced products that include Gore-Tex® shells and Windstopper® fleece (both registered with W. L. Gore & Associates, Inc.), Conduit™ shells, down parkas and technical clothing designed for specialized outdoor activities such as mountaineering, backpacking and climbing. These products are used by elite mountaineering athletes around the globe.

Our Pacific Trail-branded outerwear features functional jackets for both men and women. Pacific Trail products are focused on the consumer who demands quality and performance at an exceptional value.

Sportswear

Our sportswear products are designed to be sold alongside our outerwear and footwear products as part of our unified “head-to-toe” outfitting concept. We currently develop and distribute sportswear products under our Columbia, Mountain Hardwear, and Sorel brands.

Building on a foundation of authentic fishing and hunting shirts, we have expanded our Columbia-branded sportswear product line to include pants, hiking shorts, water sport trunks, fleece and pile products, sweaters, chinos, knit shirts, and woven shirts. Our sportswear product line appeals to both the serious outdoorsman and the more casual wearer. We also produce a separate line of Columbia-branded youth sportswear products.

For the consumer interested in trekking and adventure travel, our Titanium® sportswear line of active outdoor performance apparel offers lightweight products, many of which incorporate our Omni-ShadeTM sun protection and Omni-Dry® system of moisture management.

Our PFG® (Performance Fishing Gear) line offers a variety of products, including vests, shorts, shirts, and pants with technical features such as Omni-ShadeTM sun protection.

Mountain Hardwear-branded sportswear is focused on styles that are designed for backpacking, rock climbing and adventure sports. Many styles feature the Mountain Hardwear patented “Conical Waist,” which improves comfort and performance while wearing a backpack. Most styles use technically advanced fabrics, and the category has grown to include casual as well as performance athletic apparel.

3

Footwear

Our footwear category consists of seasonal outdoor footwear for a variety of activities. We currently develop and distribute footwear products under our Columbia, Sorel and Montrail brands. Many of our footwear brands feature designs that incorporate Omni-Tech™ waterproof/breathable construction and Tech-Lite™ advanced cushioning technology. We believe the market for footwear represents a substantial growth opportunity.

The Columbia brand of footwear offers a wide assortment of products to cover a variety of activities. We continue to focus on the active outdoor consumer in all footwear products including water, trail, hiking, cold weather casual and youth footwear. The Columbia brand of footwear is offered in several distribution channels, including footwear specialty, sports specialty, and outdoor.

The Sorel brand has been known for cold weather footwear for over forty years. We continue to capitalize on Sorel’s cold weather heritage and focus on making Sorel the leading cold weather brand for outdoor-oriented men, women and youth.

Montrail-branded footwear offers high quality and high performance products designed for trail running, adventure racing, hiking, and backpacking. We believe Montrail footwear provides a complementary extension of our portfolio of brands in the specialty outdoor market.

Accessories and Equipment

We produce a line of Columbia and Mountain Hardwear accessories that includes hats, caps, scarves, gloves, mittens and headbands to complement our outerwear and sportswear lines.

We produce a line of Mountain Hardwear equipment that includes technically-advanced tents, sleeping systems, and backpacks. These products are designed for mountaineering, ultralight backpacking and camping. Some of these product designs are patented and are considered industry standards in innovation.

We also produce a line of Columbia-branded equipment, including bags and packs.

Licensing

In 1999, we introduced a strategy to build brand awareness by licensing our trademarks across a range of product categories that complement our current offerings. Licensing enables us to develop our “head-to-toe” outfitting concept by expanding the reach of our brands to appropriate and well-defined categories. In 2007, we licensed our brands in fifteen product categories, including, among others, socks, performance base layer, leather outerwear and accessories, camping gear, eyewear, home furnishings, and bicycles.

Advertising, Marketing, and Promotion

Columbia’s multi-dimensional advertising has been designed to maximize impact on key Columbia consumers, as well as incorporate a large mix of media chosen to reach targeted audiences. Marketing, advertising and promotional programs are integral parts of our overall global go-to-market strategy. In the past year we have established a more aggressive focus on marketing with the goals of building brand equity, raising global awareness, infusing the brand with excitement and stimulating consumer demand.

Our overall advertising strategy combines ads in traditional broad-based national print and broadcast media with ads in web-based narrowcast channels and editorial-style articles in print media. Our websites educate millions of visitors each year about our products and links them directly to retailers both on and off-line. Special sweepstakes, promotions and outgoing email marketing efforts further enhance our consumers’ connection to the

4

brand. We are broadening our reach and exposure through advertising opportunities on television aimed at mass consumer appeal. In early 2008, we signed an advertising agreement with Discovery Channel in connection with our increased marketing effort. Collectively these campaigns are designed to boost consumer brand awareness and stimulate consumer demand to increase sales of our products worldwide.

Our unique, award-winning, global Columbia advertising campaign featuring our Chairman, Gertrude Boyle, in the role of cantankerous “Mother Boyle” and her son, Timothy Boyle, our President and Chief Executive Officer, as the ultimate test subject, continues to be an integral part of Columbia’s brand identity, promoting the brand message of product durability and comfort through a “Tested Tough” theme.

Sales through existing retail channels are enhanced by visual merchandising. Concept shops and focus areas located within our customers’ stores are dedicated exclusively to selling our merchandise on a year-round basis. These shops and focus areas promote a consistent brand image throughout our wholesale customer network. In addition, our cooperative advertising program provides wholesale customers an advertising allowance related to the value of their purchases when specific criteria are met.

Mountain Hardwear and Montrail brand marketing is geared toward experienced outdoor enthusiasts who purchase products primarily through outdoor specialty stores, while Sorel brand marketing targets those who work and recreate outdoors, mainly in cold weather climates.

Inventory Management

From the time of initial order through production, distribution and delivery, we manage our inventory to reduce risk. Our inventory management systems, coupled with our enterprise-wide information system, have enhanced our ability to manage our inventories by providing detailed inventory status from the time of initial factory order through shipment to our wholesale customers.

Additionally, through the use of incentive discounts we encourage early orders by our customers and we provide our customers with staggered delivery times through the spring and fall seasons. This permits our customers and us to manage inventories effectively. Through our efforts to match our purchases of inventory to the receipt of customer orders, we believe we are able to reduce the risk of overcommitting to inventory purchases. This helps us avoid significant unplanned inventory build-ups and minimizes working capital requirements. This strategy, however, does not eliminate inventory risk entirely because we build some amount of speculative inventory into our business model. Moreover, customer orders are subject to cancellation prior to shipment. In addition, a portion of our inventory is managed to support at-once and auto-replenishment orders, primarily in the sportswear category, as well as our retail expansion efforts.

Product Design

Our experienced in-house merchandising and design teams work closely with internal sales and production teams as well as with retailers, athletes and consumers to make products that are functional and durable.

We incorporate differentiated technical features into our Columbia-brand products to enhance our tiered sub-branding strategy, which encompasses three product lines. Our high-end performance products are highly technical products generally sold in specialty stores; our moderate products are technical products generally sold in sporting goods stores; and our most broadly distributed products are less technical, core products generally sold in department stores. We believe that increased differentiation of our products allows our retailer customers to better target their specific customers.

We design our products to perform well in a wide range of weather conditions and for a variety of outdoor activities. We carefully choose the appropriate fabric or insulation for each garment. Our fabrics feature optimum performance characteristics such as water resistance, breathability, weight, durability, and wicking ability. Our

5

high-end performance products include technical garments with special performance features. Our Titanium sub-branded apparel offers high performance fabrics and features our most advanced technologies. A variety of levels are offered to meet different needs of water resistance, breathability, and protection. We recently introduced our Omni-ShadeTM and TechLite® product and marketing initiatives that reinforce the outdoor authenticity of the Columbia brand. For our sportswear collections, our Omni-Shade initiative offers UPF-rated sun protection products designed to protect consumers from the harmful effects of the sun’s ultraviolet rays. Our footwear collection features TechLite® technology that integrates lightweight comfort with long-term durability.

Mountain Hardwear products feature innovative fabrics, designs and technical elements. The products are intended for extreme environments but also are appropriate for more general uses such as skiing and hiking. The outerwear line features technical fabrics such as Gore-Tex and Windstopper for shellwear and technical fleece garments. Mountain Hardwear uses its waterproof/breathable technology, Conduit, in both shell and softshell garments. Features such as external seam taping and welded construction position Mountain Hardwear as an industry leader in innovation. We acquired the Mountain Hardwear brand in 2003.

The Sorel brand is widely viewed as the preeminent cold weather footwear brand in many global markets. For over 40 years, the Sorel brand has provided consumers with high quality, waterproof and insulated cold weather footwear products. We acquired the Sorel brand in 2000 and continue to focus on offering great footwear that works equally well for winter recreation and everyday cold weather wear for consumers of all ages.

Our Montrail footwear products are specifically designed to withstand harsh conditions and heavy usage for the most demanding and critical outdoor users, while at the same time offering superior comfort for everyday activities. The products feature highly technical attributes including protection from trail hazards, stability control on uneven terrain, and traction control specifically designed for a variety of surfaces including mud, snow or wet conditions. We acquired the Montrail brand in 2006.

The Pacific Trail brand, which we acquired in 2006, has long been associated with quality garments targeted for the mass merchant and discount channels in the U.S. and Canada. This remains our strategy and we continue to actively explore a variety of design and distribution alternatives for the brand.

Sourcing and Manufacturing

Our products are produced by independent contract manufacturers. We believe that the use of independent contract manufacturers, as opposed to owning and managing our own factories, enables us to substantially limit our capital expenditures and avoid costs associated with managing a large production work force. We also believe the use of independent contract manufacturers greatly increases our production capacity, maximizes our flexibility and improves our product pricing.

We maintain fourteen manufacturing liaison offices in the Far East, and one manufacturing liaison office in Los Angeles, California. Personnel in these manufacturing liaison offices are direct employees of Columbia, and are responsible for selecting and managing our contract manufacturers. We believe that by having employees in these regions we enhance our ability to monitor factories to increase compliance with our policies, procedures, and standards related to quality, delivery, pricing, and labor practices.

Our quality assurance process is designed to ensure that our products meet the highest quality standards. Our employees monitor the quality of fabrics and other components and inspect prototypes of each product before starting production runs. In addition, our employees perform quality audits throughout the production process up to and including final shipment to our customers. We believe that our quality assurance process is an important and effective means of maintaining the quality and reputation of our products.

Contract manufacturers generally produce our apparel using one of two principal methods. In the first method, the manufacturer purchases the raw materials needed to produce the garment from suppliers that we

6

have approved, at prices and on terms negotiated by either the manufacturer or by us. The majority of our merchandise is manufactured under this type of arrangement. In the second method, sometimes referred to as “cut, make, pack, and quota” and used principally for production in China, we directly purchase the raw materials from suppliers, assure that the independent manufacturers have the necessary import quotas available, and ship the materials in a “kit,” together with patterns, samples, and most of the other necessary items, to the independent manufacturer to produce the finished garment. Although this second type of arrangement advances the timing for inventory purchases and exposes us to additional risks before a garment is manufactured, we believe that it further increases our manufacturing flexibility and frequently provides us with a cost advantage over other production methods.

We transact business on an order-by-order basis without exclusive commitments or arrangements to purchase from any single manufacturer. We believe, however, that our historical long term relationships with various manufacturers will help to ensure that adequate sources are available to produce a sufficient supply of goods in a timely manner and on satisfactory economic terms in the future.

We have from time to time had difficulty satisfying our raw material and finished goods requirements, and any similar future difficulties may adversely affect our business operations. Our four largest factory groups accounted for approximately 14% of our total global production for 2007, and a single vendor supplies substantially all of the zippers used in our products. These companies, however, have multiple factory locations, many of which are in different countries. This reduces the risk that unfavorable conditions at a single factory or location will have a material adverse effect on our business.

Sales and Distribution

Our products are sold to approximately 14,000 retailers throughout the world, ranging from specialty stores to department stores. Our strategy for continued growth is to focus on:

| • | enhancing the channel productivity of our existing customers; |

| • | leveraging our brands internationally; |

| • | further developing our existing merchandise categories; |

| • | increasing our penetration into the department store and specialty footwear channels; and |

| • | expanding the global awareness of our brands through license agreements. |

The following table presents net sales to unrelated entities and approximate percentages of net sales by geographic segment for each of the last three years (dollars in millions):

| 2007 | 2006 | 2005 | ||||||||||||||||

| Net Sales | % of Sales | Net Sales | % of Sales | Net Sales | % of Sales | |||||||||||||

| United States |

$ | 767.2 | 56.6 | % | $ | 752.0 | 58.4 | % | $ | 676.9 | 58.6 | % | ||||||

| Europe, Middle East and Africa (“EMEA”) |

287.0 | 21.1 | 272.6 | 21.2 | 243.2 | 21.0 | ||||||||||||

| Latin America and Asia Pacific (“LAAP”) |

175.7 | 13.0 | 142.9 | 11.1 | 120.9 | 10.5 | ||||||||||||

| Canada |

126.1 | 9.3 | 120.2 | 9.3 | 114.8 | 9.9 | ||||||||||||

| Total |

$ | 1,356.0 | 100.0 | % | $ | 1,287.7 | 100.0 | % | $ | 1,155.8 | 100.0 | % | ||||||

See Note 16 of Notes to Consolidated Financial Statements for net sales to unrelated entities, income before income tax, interest income (expense), income tax expense (benefit), depreciation and amortization expense and identifiable assets by geographic segment.

7

United States and Canada

Approximately 39% of the retailers that offer our products worldwide are located in the United States and Canada. Sales in these two countries accounted for 65.9% of our net sales for 2007.

Columbia, Sorel, Montrail, and Pacific Trail products are primarily sold through a combination of in-house and independent sales agents that in turn work with retail accounts varying in size from single specialty store operations to large chains made up of many stores in several locations.

Mountain Hardwear products are primarily sold through independent sales agencies that work with a variety of retail accounts that are primarily focused on smaller specialty outdoor and ski shops across the United States. Mountain Hardwear products are also sold through select specialty chain stores and catalog companies that feature high end outdoor equipment and apparel.

Our flagship company-owned retail store in Portland, Oregon is designed to create a distinctive “Columbia” environment, reinforcing the active and outdoor image of the Columbia brand. In addition, we use this store to test new marketing and merchandising techniques. We also operate fourteen outlet stores in various locations throughout North America. These outlet stores are primarily designed to sell excess and distressed inventory without adversely affecting our retail accounts.

In 2007 we introduced a retail expansion strategy designed to improve inventory management and distribution of excess and end-of-season products in the U.S. with minimal disruption to our wholesale distribution channels. This strategy involves opening approximately 15 new outlet stores in key U.S. outlet centers during each of the next few years, building on our base of existing outlet stores. In addition, as part of our increased focus on consumer demand creation, we plan to open several new first-line retail stores for our brands in key metropolitan markets in order to provide a comprehensive environment to communicate key marketing initiatives, breadth of assortments and expert service levels expected from demanding consumers.

We inspect, sort, pack and ship the majority of our products sold to United States retailers from our Rivergate Distribution Center, which consists of approximately 850,000 square feet located in Portland, Oregon, and from our 4 Star Distribution Center, which consists of approximately 520,000 square feet located in Robards, Kentucky. We completed an upgrade to our Rivergate Distribution Center in April 2007.

We handle Canadian distribution from a leased warehouse in Strathroy, Ontario. We are also constructing additional warehouse space near our leased warehouse to accommodate future growth.

In some instances, we arrange to have products shipped directly from our independent manufacturers to customer-designated facilities in the United States and Canada.

EMEA

Our European headquarters is located in Geneva, Switzerland and we have sales offices in France, Germany, Italy, the United Kingdom, Switzerland, and the Netherlands. We sell our products directly to approximately 5,900 retailers in Western European countries.

We distribute our apparel and footwear products in direct markets in Europe through our distribution center in Cambrai, France, which consists of approximately 577,000 square feet. We completed the expansion of this facility in January 2007.

We also operate two outlet stores in Europe: one in France and one in Spain.

In several other countries throughout the EMEA region, we sell our products to independent distributors. These distributors service retail customers in locations such as Russia and portions of Europe, among others. The vast majority of sales to our EMEA distributors are factory-direct shipments.

8

LAAP

We sell our products in Japan through a combination of wholesalers and retailers, including our own direct retail operations. We distribute our products in Japan through a warehouse that is owned and operated by an independent logistics company located near Tokyo. We sell our products in Korea through a combination of wholesalers, franchisees, and retailers, including our own direct retail operations. Korean distribution is conducted from a leased warehouse near Seoul.

In several other countries throughout LAAP, we sell our products to independent distributors. These distributors service retail customers in locations such as Australia, New Zealand, South America, and China, among others. The vast majority of sales to our LAAP distributors are factory-direct shipments.

Intellectual Property

We own many trademarks, including Columbia® , Columbia Sportswear Company®, Convert®, Sorel®, Bugaboo®, Bugabootoo®, Omni-ShadeTM, Omni-Tech®, GRT®, Omni-Grip®, Columbia Interchange System®, Titanium®, Mountain Hardwear®, Montrail®, Pacific Trail®, the Columbia diamond shaped logo and arrow-circle design, the Mountain Hardwear nut logo and the Sorel polar bear logo. Our trademarks, many of which are registered or subject to pending applications in the United States and other nations, are used on a variety of goods, including apparel, footwear, equipment and licensed products. We believe that our trademarks are valuable and provide consumers with an assurance that the product being purchased is of high quality and provides good value. We also place significant value on product designs (the overall appearance and image of our products) that, along with trademarks, distinguish our products in the marketplace. We protect these proprietary rights and frequently take action to prevent counterfeit reproductions or other infringing activity. In the past we have successfully resolved conflicts over proprietary rights through legal action and negotiated settlements. As we expand our operations in geographic scope and product categories, we anticipate intellectual property disputes will increase as well, making it more expensive and challenging to establish and protect our proprietary rights and to defend against claims of infringement by others.

Seasonality of Business

Our business is affected by the general seasonal trends common to the outdoor apparel industry, with sales and profits highest in the third calendar quarter. Our products are marketed on a seasonal basis, with product sales mix weighted substantially toward the fall season. Results of operations in any period should not be considered indicative of the results to be expected for any future period. Sales of our products are subject to substantial cyclical fluctuation and impacts from unseasonable weather conditions. Sales tend to decline in periods of recession or uncertainty regarding future economic prospects that affect consumer spending, particularly on discretionary items. This cyclicality and any related fluctuation in consumer demand could have a material adverse effect on our results of operations, cash flows and financial position.

Backlog

We typically receive the bulk of our orders for each of the fall and spring seasons by March 31 and September 30, respectively. A variety of factors correspond to these dates, including the timing of our order deadlines, the timing of our receipt of orders, and the timing of our shipments. As a result, our backlog at March 31 and September 30 is a more meaningful indicator of future sales than our backlog at December 31. Accordingly, we disclose our backlog at March 31 and at September 30 in our Quarterly Reports on Form 10-Q for those respective periods, rather than at December 31. Generally, orders are subject to cancellation prior to the date of shipment.

Competition

The active outerwear, sportswear and footwear segments of the apparel industry are highly competitive and we believe that this competition will increase. Some of our competitors are substantially larger and have greater

9

financial, distribution, marketing and other resources than we do. We believe that the primary competitive factors in the market for active outerwear, sportswear, and footwear are price, brand name, functionality, durability and style and that our product offerings are well-positioned within the market. In many cases, our most significant competition comes from our own retail customers that manufacture and market clothing and footwear under their own private labels. In addition, our licensees operate in very competitive markets, such as those for watches, leather outerwear, and socks. We encounter substantial competition in the active outerwear and sportswear business from, among others, The North Face, Inc. (VF Corporation), Marmot Mountain Ltd., Spyder Active Sports, Inc., Woolrich Woolen Mills, Inc., The Timberland Company, Carhartt, Inc., Patagonia Corporation, Helly Hansen A/S, Merrell (Wolverine Worldwide Inc.), Skis Rossignol S.A. (Quiksilver, Inc.), and Burton Snowboards. In addition, we compete with major sports apparel companies, such as NIKE, Inc., adidas AG, and Under Armour, Inc., and with fashion-oriented competitors, such as Polo Ralph Lauren Corporation and IZOD (Phillips-Van Heusen Corporation). Our footwear line competes with, among others, The North Face, Timberland, NIKE ACG, adidas AG, Merrell, Salomon, Teva (Deckers Outdoor Corporation), KEEN, Inc., Crocs Inc., and Kamik (Genfoot, Inc.). Many of these companies have global operations and compete with us in Europe and Asia. In Europe we also face competition from brands such as Berghaus Limited of the United Kingdom, Jack Wolfskin Ausrustung Fur Draussen GmbH & Co Kgaa of Germany, Lafuma S.A. of France, and Helly Hansen of Scandinavia as well as many other regional brands. In Asia our competition is from brands such as The North Face, Hokurikv MontBell and Patagonia among others.

Mountain Hardwear equipment (tents and sleeping bags) competes directly with such companies as The North Face, Sierra Designs (American Recreational Products), Kelty (American Recreational Products), Marmot, Arc’ Teryx Equipment, Inc. (Salomon USA) and other smaller specialized brands worldwide. Columbia and Mountain Hardwear bags and packs compete directly with JanSport, Inc., The North Face, Osprey Packs, Inc., Eastpak, High Sierra Sport Company, and other bag and pack brands worldwide.

Credit and Collection

We extend credit to our customers based on an assessment of a customer’s financial condition, generally without requiring collateral. To assist in the scheduling of production and the shipping of seasonal products, we offer customers discounts for placing pre-season orders and extended payment terms for taking delivery before the peak shipping season. These extended payment terms increase our exposure to the risk of uncollectible receivables. In some markets and with some customers we use credit insurance to minimize our risk of credit loss. Some of our significant customers have had financial difficulties in the past, and future financial difficulties of our customers may have a material adverse effect on our business.

Government Regulation

Many of our imports are subject to existing or potential governmental tariff and non-tariff barriers to trade, such as import duties and quotas that may limit the quantity of various types of goods that may be imported into the United States and other countries. These trade barriers often represent a material portion of the cost of the merchandise. Our products are also subject to safety and environmental regulations, which are increasingly restrictive and complex. Although we diligently monitor these trade restrictions, the United States or other countries may impose new or adjusted quotas, duties, safety requirements, material restrictions, or other restrictions or regulations, any of which may have a material adverse effect on our business.

Employees

At December 31, 2007 we had the equivalent of 3,057 full-time employees. Of these employees, 1,544 were based in the United States, 1,090 in Asia, 303 in Europe and 120 in Canada.

Available Information

We file with the Securities and Exchange Commission (“SEC”) our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and all amendments to those reports, proxy statements and

10

registration statements. You may read and copy any material we file with the SEC at the SEC’s Public Reference Room at 100 F Street, NE, Washington, D.C. 20549. You may also obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. In addition, the SEC maintains an internet site at http://www.sec.gov that contains reports, proxy and information statements, and other information regarding issuers, including us, that file electronically. We make available free of charge on or through our website at www.columbia.com our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to these reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act as soon as reasonably practicable after we file these materials with the SEC.

| Item 1A. | RISK FACTORS |

In addition to the other information contained in this Form 10-K, the following risk factors should be considered carefully in evaluating our business. Our business, financial condition, or results of operations may be materially adversely affected by any of these risks. Please note that additional risks not presently known to us or that we currently deem immaterial may also impair our business and operations.

We May be Adversely Affected by Weather Conditions

Our business is adversely affected by unseasonable weather conditions. Sales of our outerwear and cold weather footwear are dependent in part on the weather and may decline in years in which weather conditions do not favor the use of these products. For example, in some fall seasons in the past, unseasonably warm weather in the United States caused customers to delay, and in some cases reduce or cancel, orders for our outerwear, which had an adverse effect on our net sales and profitability. Periods of unseasonably warm weather in the fall or winter or unseasonably cold or wet weather in the spring may have a material adverse effect on our results of operations and financial condition. Inventory accumulation by retailers resulting from unseasonable weather in one season may negatively affect orders in future seasons, which may have a material adverse effect on our results of operations and financial condition in future periods.

We May be Adversely Affected by an Economic Downturn or Economic Uncertainty

Sales of our products are subject to substantial cyclical fluctuation. Consumer demand for our products may not reach our growth targets, or may decline, when there is an economic downturn or economic uncertainty in our key markets, particularly markets in North America and Europe. For example, a slower economy in the United States is creating additional uncertainties for our customers and our business, similar to that which we experienced in 2002 and 2003. Continued volatility in the global oil markets has resulted in rising fuel prices, which shipping companies may pass on to us. Because we price our products to our customers in advance and external cost increases may be difficult to anticipate, we may not be able to pass these increased costs on to our customers. Rising oil prices and interest rates may also adversely affect consumer demand. Our investment portfolio is subject to a number of risks and uncertainties. Changes in market conditions, such as those that accompany an economic downturn or economic uncertainty, may negatively affect the value of our investment portfolio, perhaps significantly. Our sensitivity to economic cycles and any related fluctuation in consumer demand and rising shipping and other costs may have a material adverse effect on our results of operations and financial condition.

Our International Operations Involve Many Risks

We are subject to the risks generally associated with doing business abroad. These risks include foreign laws and regulations, foreign consumer preferences, political unrest, disruptions or delays in shipments and changes in economic conditions in countries in which we manufacture or sell products. In addition, disease outbreaks, terrorist acts and United States military operations have increased the risks of doing business abroad. These factors, among others, may affect our ability to sell products in international markets, our ability to manufacture products or procure materials, and our cost of doing business. If any of these or other factors make the conduct of business in a particular country undesirable or impractical, our business may be materially and adversely affected.

11

As a global company, we determine our income tax liability in various competing tax jurisdictions based on a careful analysis and interpretation of local tax laws and regulations. This analysis requires a significant amount of judgment and estimation and is often based on certain assumptions about the future actions of the local tax authorities. Such determinations are the subject of periodic domestic and foreign tax audits. Although we accrue for uncertain tax positions, our accrual may be insufficient to satisfy unfavorable findings, which by their nature cannot be predicted with certainty. Unfavorable audit findings and tax rulings may result in payment of taxes, fines and penalties for prior period and higher tax rates in future periods, which may have a material adverse effect on our results of operations and financial condition.

In addition, many of our imported products are subject to duties, tariffs or quotas that affect the cost and quantity of various types of goods imported into the United States or into our other sales markets. For example, the European Commission recently imposed additional duties on certain leather footwear imported into Europe from Vietnam and China. These duties may significantly affect the sale of our footwear in Europe. Any country in which our products are produced or sold may eliminate, adjust or impose new quotas, duties, tariffs, antidumping penalties or other charges or restrictions, any of which may have a material adverse effect on our results of operations and financial condition.

We May be Adversely Affected by the Financial Health of Retailers

We extend credit to our customers based on an assessment of a customer’s financial condition, generally without requiring collateral. To assist in the scheduling of production and the shipping of seasonal products, we offer customers discounts for placing pre-season orders and extended payment terms for taking delivery before the peak shipping season. These extended payment terms increase our exposure to the risk of uncollectible receivables. In addition, we face increased risk of order reduction or cancellation when dealing with financially ailing retailers or retailers struggling with economic uncertainty. Some of our significant customers have had financial difficulties in the past, which in turn have had an adverse effect on our business. A slowing economy in our key markets may also have an adverse effect on the financial health of our customers, which may in turn have a material adverse effect on our results of operations and financial condition.

We Operate in Very Competitive Markets

The markets for outerwear, sportswear, footwear, related accessories and equipment are highly competitive, as are the markets for our licensed products. In each of our geographic markets, we face significant competition from global and regional branded apparel, footwear, accessories and equipment companies. Retailers who are our customers often pose our most significant competitive threat by marketing apparel, footwear and equipment under their own labels. For example, in 2006 and 2007 our European business was negatively affected by a key customer’s decision to expand its private label program, which resulted in reduced outerwear and footwear orders from that key customer. We also compete with other companies for the production capacity of independent manufacturers that produce our products and for import quota capacity. Many of our competitors are significantly larger than us, have substantially greater financial, distribution, marketing and other resources than we have, and have achieved greater recognition for their products than we have. Increased competition may result in reductions in display areas in retail locations, reductions in sales, or reductions in our profit margins, any of which may have a material adverse effect on our results of operations and financial condition.

We May be Adversely Affected by Retailer Consolidation

When retailers combine their operations through mergers, acquisitions, or other transactions, their consolidated order volume may decrease while their bargaining power and the competitive threat they pose by marketing products under their own label may increase. Some of our significant customers have consolidated their operations in the past, which in turn has had a negative effect on our business. We expect retailer consolidation to continue, which may have a material adverse effect on our results of operations and financial condition.

12

We Face Risks Associated with Consumer Preferences and Fashion Trends

Changes in consumer preferences or consumer interest in outdoor activities may have a material adverse effect on our business. In addition, although we believe that our products have not been significantly affected by past fashion trends, changes in fashion trends may have a greater impact as we expand our offerings to include more product categories in more geographic areas. We also face risks because our business requires us to anticipate consumer preferences. Our decisions about product designs often are made far in advance of consumer acceptance. Although we try to manage our inventory risk through early order commitments by retailers, we must generally place production orders with manufacturers before we have received all of a season’s orders, and orders may be cancelled by retailers before shipment. If we fail to anticipate and respond to consumer preferences, we may have lower sales, excess inventories and lower profit margins, any of which may have a material adverse effect on our results of operations and financial condition.

Our Success Depends on Our Use of Proprietary Rights

Our registered and common law trademarks have significant value and are important to our ability to create and sustain demand for our products. We also place significant value on our trade dress, the overall appearance and image of our products. From time to time, we discover products that are counterfeit reproductions of our products or that otherwise infringe on our proprietary rights. Counterfeiting activities typically increase as brand recognition increases, especially in markets outside the United States. Increased instances of counterfeit manufacture and sales of these products may adversely affect our sales and our brand and result in a shift of consumer preference away from our products. The actions we take to establish and protect trademarks and other proprietary rights may not be adequate to prevent imitation of our products by others or to prevent others from seeking to block sales of our products as violations of proprietary rights. In markets outside of the United States, it may be more difficult for us to establish our proprietary rights and to successfully challenge use of those rights by other parties. We also license our proprietary rights to third parties. Failure to choose appropriate licensees and licensed product categories may dilute or harm our brand image. Actions or decisions in the management of our intellectual property portfolio may affect the strength of the brand, which may in turn have a material adverse effect on our results of operations and financial condition.

Although we have not been materially inhibited from selling products in connection with trademark and trade dress disputes, as we extend our brand into new product categories and new product lines and expand the geographic scope of our marketing, we may become subject to litigation based on allegations of the infringement of intellectual property rights of third parties including third party trademark, copyright and patent rights. Future litigation also may be necessary to defend us against such claims or to enforce and protect our intellectual property rights. Any intellectual property litigation may be costly and may divert management’s attention from the operation of our business. Adverse determinations in any litigation may result in the loss of our proprietary rights, subject us to significant liabilities or require us to seek licenses from third parties, which may not be available on commercially reasonable terms, if at all. This may have a material adverse effect on our results of operations and financial condition.

Our Success Depends on Our Distribution Facilities

Our ability to meet customer expectations, manage inventory, complete sales and achieve objectives for operating efficiencies depends on the proper operation of our existing distribution facilities, the development or expansion of additional distribution capabilities and the timely performance of services by third parties (including those involved in shipping product to and from our distribution facilities). In the United States, we rely primarily on our distribution centers in Portland, Oregon and Robards, Kentucky; in Canada, we rely primarily on our distribution center in Strathroy, Ontario; and in Europe we rely primarily on our distribution center in Cambrai, France.

Our distribution facilities in the United States and France are highly automated, which means that their operations are complicated and may be subject to a number of risks related to computer viruses, the proper operation of software and hardware, electronic or power interruptions, and other system failures. Risks associated with upgrading or expanding these facilities may significantly disrupt or increase the cost of our operations.

13

Our distribution facilities may also be interrupted by disasters, such as earthquakes (which are known to occur in the Northwestern United States) or fires. We maintain business interruption insurance, but it may not adequately protect us from the adverse effect that may be caused by significant disruptions in our distribution facilities.

Our Success Depends on Our Information Systems

Our business is increasingly reliant on information technology. Information systems are used in all stages of our production cycle, from design to distribution and sales, and are used as a method of communication between employees, with our subsidiaries and liaison offices overseas, as well as with our customers. We also rely on our information systems to allocate resources and forecast operating results. System failures, breach of confidential information, or service interruptions may occur as the result of a number of factors, including computer viruses, hacking or other unlawful activities by third parties, disasters, or our failure to properly protect, repair, maintain, or upgrade our systems. Any breach or interruption of critical business information systems may have a material adverse affect on our results of operations and financial condition.

Our Success Depends on Our Growth Strategies

We face many challenges in implementing our growth strategies. For example, our expansion into international markets involves countries where we have little sales or distribution experience and where our brands are not yet widely known. Expanding our product categories involves, among other things, gaining experience with new brands and products, gaining consumer acceptance, and establishing and protecting intellectual property rights. Increasing sales to department stores and improving the sales productivity of our customers will each depend on various factors, including strength of our brand names, competitive conditions, our ability to manage increased sales and future expansion, the availability of desirable locations and the negotiation of terms with retailers. Future terms with customers may be less favorable to us than those under which we now operate. Large retailers in particular increasingly seek to transfer various costs of business to their vendors, such as the cost of lost profits from product price markdowns. Our strategy to open and operate additional outlet and first-line retail stores also involves many challenges and risks. The success of our retail initiative depends on our ability to adapt our internal processes to facilitate direct-to-consumer sales, to effectively manage retail store inventory, to hire, retain and train personnel capable of managing a retail operation, to identify and negotiate favorable terms for new retail locations, and to effectively manage construction and opening of stores in multiple locations.

To implement our business strategy, we must manage growth effectively. We must continue to modify various aspects of our business, to maintain and enhance our information systems and operations to respond to increased demand and to attract, retain and manage qualified personnel. Growth may place an increasing strain on management, financial, product design, marketing, distribution and other resources, and we may have operating difficulties as a result. For example, in recent years, we have undertaken a number of new initiatives that require significant management attention and corporate resources, including the development or expansion of distribution facilities on two continents, the acquisition of the Sorel and Pacific Trail brands, and the acquisition and integration of Mountain Hardwear, Inc. and the Montrail brand. This growth involves many risks and uncertainties that, if not managed effectively, may have a material adverse effect on our results of operations and financial condition.

We May be Adversely Affected by Currency Exchange Rate Fluctuations

Although we generally purchase products in U.S. dollars, the cost of these products, which are generally produced overseas, may be affected by changes in the value of the relevant currencies. Price increases caused by currency exchange rate fluctuations may make our products less competitive or have an adverse effect on our margins. Our international revenues and expenses generally are derived from sales and operations in foreign currencies, and these revenues and expenses may be materially affected by currency fluctuations, including

14

amounts recorded in foreign currencies and translated into U.S. dollars for consolidated financial reporting. Currency exchange rate fluctuations may also disrupt the business of the independent manufacturers that produce our products by making their purchases of raw materials more expensive and more difficult to finance. As a result, foreign currency fluctuations may have a material adverse effect on our results of operations and financial condition.

We May be Adversely Affected by Labor Disruptions

Our business depends on our ability to source and distribute products in a timely manner. Labor disputes at factories, shipping ports, transportation carriers, or distribution centers create significant risks for our business, particularly if these disputes result in work slowdowns, lockouts, strikes, or other disruptions during our peak manufacturing and importing seasons, and may have a material adverse effect on our business, potentially resulting in cancelled orders by customers, unanticipated inventory accumulation, and reduced revenues and earnings.

We Depend on Independent Manufacturers

Our products are produced by independent manufacturers worldwide. We do not operate or own any production facilities. Although we enter into a number of purchase order commitments each season, we generally do not maintain long-term manufacturing contracts. Because of these factors, manufacturing operations may fail to perform as expected or our competitors may obtain production or quota capacities that effectively limit or eliminate the availability of these resources to us. If a manufacturer fails to ship orders in a timely manner or to meet our standards or if we are unable to obtain necessary production or quota capacities, we may miss delivery deadlines, or incur additional costs, which may result in cancellation of orders, refusal to accept deliveries, a reduction in purchase prices, or increased costs, any of which may have a material adverse effect on our business. Reliance on independent manufacturers also creates quality control risks. A failure in our quality control program may result in diminished product quality, which may result in increased order cancellations and returns, decreased consumer demand for our products, or product recalls, any of which may have a material adverse affect on our results of operations and financial condition. Finally, if a manufacturer violates labor or other laws, or engages in practices that are not generally accepted as ethical in our key markets, we may be subject to significant negative publicity, consumer demand for our products may decrease, and under some circumstances we may be subject to liability for the manufacturer’s practices, any of which may have a material adverse effect on our results of operations and financial condition.

We Depend on Key Suppliers

Some of the materials that we use may be available from only one source or a very limited number of sources. For example, some specialty fabrics are manufactured to our specification by one source or a few sources and zippers are supplied by one manufacturer. From time to time, we have difficulty satisfying our raw material and finished goods requirements. Although we believe that we can identify and qualify additional manufacturers to produce these materials as necessary, there are no guarantees that additional manufacturers will be available. In addition, depending on the timing, any changes may result in increased costs or production delays, which may have a material adverse effect on our results of operations and financial condition.

Our Advance Purchases of Products May Result in Excess Inventories

To minimize our purchasing costs, the time necessary to fill customer orders and the risk of non-delivery, we place orders for our products with manufacturers prior to receiving all of our customers’ orders and we maintain an inventory of various products that we anticipate will be in greater demand. We may not be able to sell the products we have ordered from manufacturers or that we have in our inventory. Customers are allowed to cancel an order prior to shipment with sufficient notice. Inventory levels in excess of customer demand may result in inventory write-downs and the sale of excess inventory at discounted prices, which may have a material adverse effect on our results of operations and financial condition.

15

We Depend on Key Personnel

Our future success will depend in part on the continued service of key personnel, particularly Timothy Boyle, our President and Chief Executive Officer, and Gertrude Boyle, our Chairman and widely-recognized advertising spokesperson. Our future success will also depend on our ability to attract and retain key managers, designers, sales people and others. We face intense competition for these individuals worldwide, and there is a significant concentration of well-funded apparel and footwear competitors in and around Portland, Oregon (including NIKE, Inc. and adidas AG). We may not be able to attract qualified new employees or retain existing employees, which may have a material adverse effect on our results of operations and financial condition.

Our Business Is Affected by Seasonality

Our results of operations are likely to continue to fluctuate significantly from period to period. Our products are marketed on a seasonal basis; our results of operations for the quarter ended September 30 in the past have been much stronger than the results for the other quarters. This seasonality, along with other factors that are beyond our control, and that are discussed elsewhere in this section, may adversely affect our business and cause our results of operations to fluctuate. Our operating margins are also sensitive to a number of factors that are beyond our control, including shifts in product sales mix, geographic sales trends, and currency exchange rate fluctuations, all of which we expect to continue as we expand our product offerings and geographic penetration. Results of operations in any period should not be considered indicative of the results to be expected for any future period.

We Face Risks of Product Liability and Warranty Claims

Our products are used in outdoor activities, sometimes in severe conditions. Although we have not incurred any significant expense as the result of product recalls or product liability claims, recalls or claims in the future may have a material adverse effect on our results of operations and financial condition. Some of our products carry warranties for defects in quality and workmanship. We maintain a warranty reserve for future warranty claims, but the actual costs of servicing future warranty claims may exceed the reserve, which may also have a material adverse effect on our results of operations and financial condition.

Our Common Stock Price May Be Volatile

The price of our common stock has fluctuated substantially since our initial public offering. Our common stock is traded on the NASDAQ Global Select Market, which is likely to continue to have significant price and volume fluctuations that may adversely affect the market price of our common stock without regard to our operating performance. Factors such as fluctuations in financial results, variances from financial market expectations, changes in earnings estimates by analysts, or announcements by us or our competitors may also cause the market price of our common stock to fluctuate, perhaps substantially.

Insiders Control a Majority of Our Common Stock and May Sell Shares

Three shareholders—Timothy Boyle, Gertrude Boyle and Sarah Bany—beneficially own a majority of our common stock. As a result, if acting together, they can effectively control matters requiring shareholder approval without the cooperation of other shareholders. Shares held by these three insiders are available for resale, subject to the requirements of, and the rules under, the Securities Act of 1933 and the Securities Exchange Act of 1934. The sale or the prospect of the sale of a substantial number of these shares may have an adverse effect on the market price of our common stock.

| Item 1B. | UNRESOLVED STAFF COMMENTS |

None.

16

| Item 2. | PROPERTIES |

Following is a summary of principal properties owned or leased by us.

| Corporate Headquarters: | U.S. Distribution Facilities: | |

| Portland, Oregon (1 location)—owned | Portland, Oregon (1 location)—owned | |

| Canadian Operation (1): | Robards, Kentucky (1 location)—owned | |

| Strathroy, Ontario (1 location)—leased |

Europe Distribution Facility: | |

| Cambrai, France (1 location)—owned |

| (1) | Lease expires in December 2011. |

| Item 3. | LEGAL PROCEEDINGS |

From time to time in our normal course of business we are a party to various legal claims, actions and complaints. Currently, we do not have any pending litigation that we consider material.

| Item 4. | SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS |

None.

| Item 4A. | EXECUTIVE OFFICERS AND KEY EMPLOYEES OF THE REGISTRANT |

The following table sets forth our executive officers and certain key employees.

| Name |

Age | Position | ||

| Gertrude Boyle |

83 | Chairman of the Board (1) | ||

| Timothy P. Boyle |

58 | President, Chief Executive Officer, Director (1) | ||

| Patrick D. Anderson |

50 | Vice President and Chief Operating Officer, Assistant Secretary (1) | ||

| Kerry W. Barnes |

56 | Vice President of Retail | ||

| Peter J. Bragdon |

45 | Vice President and General Counsel, Secretary (1) | ||

| Sherrie M. Curtin |

52 | Vice President of Women’s and Youth Apparel | ||

| Thomas B. Cusick |

40 | Vice President and Corporate Controller | ||

| Daniel G. Hanson |

49 | Vice President of Marketing | ||

| Mark N. Koppes |

45 | Vice President of Men’s Apparel | ||

| Michael W. McCormick |

45 | Vice President of Sales (1) | ||

| Mark Nenow |

50 | Vice President of Footwear | ||

| Susan G. Popp |

52 | Vice President of Human Resources (1) | ||

| Mark J. Sandquist |

48 | Vice President of Apparel and Equipment (1) | ||

| Bryan L. Timm |

44 | Vice President and Chief Financial Officer, Treasurer (1) | ||

| William Tung |

43 | Vice President of International Sales and Operations (1) | ||

| Patrick J. Werner |

52 | Vice President of Global Apparel Manufacturing |

| (1) | These individuals are considered Executive Officers of Columbia. |

Gertrude Boyle has served as Chairman of the Board of Directors since 1983. Columbia was founded by her parents in 1938 and managed by her husband, Neal Boyle, from 1964 until his death in 1970. Mrs. Boyle also served as our President from 1970 to 1988. Mrs. Boyle is Timothy P. Boyle’s mother.

Timothy P. Boyle joined Columbia in 1971 as General Manager and has served as President and Chief Executive Officer since 1988. He has been a member of the Board of Directors since 1978. Mr. Boyle is also a member of the Board of Directors of Northwest Natural Gas Company and Widmer Brothers Brewing Company. Mr. Boyle is Gertrude Boyle’s son.

17

Patrick D. Anderson joined Columbia in June 1992 as Manager of Financial Reporting, became Corporate Controller in August 1993, and was appointed Chief Financial Officer in December 1996. In May 2001, Mr. Anderson was appointed Vice President of Finance and Administration as well as Assistant Secretary and served in this position until July 2002 when Mr. Anderson was named Vice President and Chief Operating Officer. From 1985 to 1992, Mr. Anderson was an accountant with Deloitte & Touche LLP.

Kerry W. Barnes joined Columbia in January 2007 as Vice President of Retail. From 2000 to 2006, Mr. Barnes served as the U.S. Director of Retail Stores for adidas AG. From 1981 to 2000, Mr. Barnes held various retail positions at Foot Locker, Inc. including Director of Outlet Sales and Regional Retail Vice President.

Peter J. Bragdon became Vice President and General Counsel, Secretary of Columbia in July 2004. Previously, from 1999 to January 2003, Mr. Bragdon served as Senior Counsel and Director of Intellectual Property for Columbia. Mr. Bragdon served as Chief of Staff in the Oregon Governor’s office from January 2003 through June 2004. From 1993 to 1999, Mr. Bragdon was an attorney in the corporate securities and finance group at Stoel Rives LLP. Mr. Bragdon served as Special Assistant Attorney General for the Oregon Department of Justice for seven months in 1996.

Sherrie M. Curtin joined Columbia in 1997 as Key Account Sales Manager and held various management positions in both the apparel sales and merchandising divisions until November 2006 when she was promoted to Vice President of Women’s and Youth Apparel. Prior to joining Columbia, Ms. Curtin held a merchandise management position at adidas AG from 1996 to 1997. From 1976 to 1996, Mrs. Curtin held various management positions in footwear and apparel for G. I. Joe’s, Inc.

Thomas B. Cusick joined Columbia in September 2002 as Corporate Controller and was named Vice President and Corporate Controller in March 2006. From 1995 to 2002, Mr. Cusick worked for Cadence Design Systems (and OrCAD, a company acquired by Cadence in 1999), which operates in the electronic design automation industry, in various financial management positions. From 1990 to 1995, Mr. Cusick was an accountant with KPMG LLP.

Daniel G. Hanson joined Columbia in September 1989 and held various management positions in sales and marketing until 1996, when he became Director of Marketing Communications. In March 2006 Mr. Hanson was named Vice President of Marketing. From 1982 to 1989 Mr. Hanson worked for Helly-Hansen, where he served as United States Marketing Manager from 1986 to 1989.

Mark N. Koppes joined Columbia in August 2005 as General Manager, Men’s Apparel. In November 2006, he was promoted to Vice President of Men’s Apparel. Prior to Columbia, Mr. Koppes worked at NIKE, Inc. for 15 years in various positions including Product Line Manager, Apparel Merchandise Manager, Marketing Director, Apparel Business Director, Global Merchandise Director and Men’s Apparel General Manager.

Michael W. McCormick joined Columbia in July 2006 as Vice President of Sales. From 2003 to 2006, Mr. McCormick served as Chief Marketing Officer for Golf Galaxy, Inc. From 2000 to 2002, Mr. McCormick served as Executive Vice President—Global Sales for Callaway Golf Company, and from 1992 to 2000, Mr. McCormick worked for NIKE, Inc. in various sales management positions, including Director of National Sales.

Mark Nenow joined Columbia in May 2007 as Vice President of Footwear. From 2006 to 2007, Mr. Nenow served as Vice President of Global Footwear Merchandising at Brooks Sports. From 1995 to 2006, Mr. Nenow was at NIKE, Inc. where he held various product line management positions in the running and outdoor categories. Prior to his footwear career, Mark was a professional track and field athlete and held the American track record for the 10,000 meters from 1986 to 2003.

18

Susan G. Popp joined Columbia in April 1997 as Human Resources Manager and in May of 2004 was named Human Resources Director. In March 2006, Ms. Popp was named Vice President of Human Resources. Prior to joining Columbia, Ms. Popp held Human Resource positions at NIKE, Inc. from 1996 to 1997; at Avia from 1994 to 1996; and at Blue Cross and Blue Shield of Oregon from 1981 to 1993.

Mark J. Sandquist joined Columbia in March 1995 as Senior Merchandiser of Men’s and Women’s Sportswear and in August 2000 was named General Manager—Sportswear Merchandising. In July 2004, Mr. Sandquist was named Vice President of Apparel and Equipment. From 1985 to 1995, Mr. Sandquist held various management positions for Unionbay Sportswear.

Bryan L. Timm joined Columbia in June 1997 as Corporate Controller and was named Chief Financial Officer in July 2002. In 2003 Mr. Timm was also named Vice President and Treasurer. From 1991 to 1997 Mr. Timm held various financial management positions for Oregon Steel Mills, Inc. From 1986 to 1991, Mr. Timm was an accountant with KPMG LLP. Mr. Timm is a member of the Board of Directors of Umpqua Holdings Corporation.

William Tung joined Columbia in September 2003 and was named Vice President of International Sales and Operations in December 2004. From 2002 to 2003, Mr. Tung worked for The Body Shop International PLC as Regional Director of North Asia. He was employed by The Rockport Company from 1994 to 2002 where he served in a variety of capacities, most recently as Vice President of Europe. From 1991 to 1994, Mr. Tung worked for Prince Racquet Sports (a division of Benetton Sportsystems) as Sales and Marketing Manager of Asia-Pacific.

Patrick J. Werner joined Columbia in April 2004 as the Director of Apparel Sportswear Sourcing. In November 2006, he was promoted to Vice President of Global Apparel Manufacturing. Prior to Columbia, Mr. Werner held several key apparel manufacturing and labor compliance roles at NIKE, Inc., where he worked from 1981 until 2004.

19

PART II

| Item 5. | MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

Our common stock is listed on the NASDAQ Global Select Market and trades under the symbol “COLM.” At February 15, 2008, we had approximately 184 shareholders of record.

Following are the quarterly high and low closing prices for our Common Stock for the years ended December 31, 2007 and 2006:

| HIGH | LOW | DIVIDENDS DECLARED | |||||||

| 2007 |

|||||||||

| First Quarter |

$ | 66.75 | $ | 54.69 | $ | 0.14 | |||

| Second Quarter |

$ | 70.38 | $ | 62.50 | $ | 0.14 | |||

| Third Quarter |

$ | 69.68 | $ | 55.31 | $ | 0.14 | |||

| Fourth Quarter |

$ | 56.77 | $ | 43.55 | $ | 0.16 | |||

| 2006 |

|||||||||

| First Quarter |

$ | 54.54 | $ | 45.35 | — | ||||

| Second Quarter |

$ | 57.31 | $ | 44.96 | — | ||||

| Third Quarter |

$ | 56.76 | $ | 43.60 | — | ||||

| Fourth Quarter |

$ | 61.32 | $ | 52.77 | $ | 0.14 | |||

Since the completion of our initial public offering in April 1998 through the third quarter of 2006, we did not declare any dividends. We declared our first quarterly dividend in November 2006. Our current dividend policy is dependent on our earnings, capital requirements, financial condition, restrictions imposed by our credit agreements, and other factors considered relevant by our Board of Directors. For various restrictions on our ability to pay dividends, see Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations, and Note 6 of Notes to Consolidated Financial Statements.

20

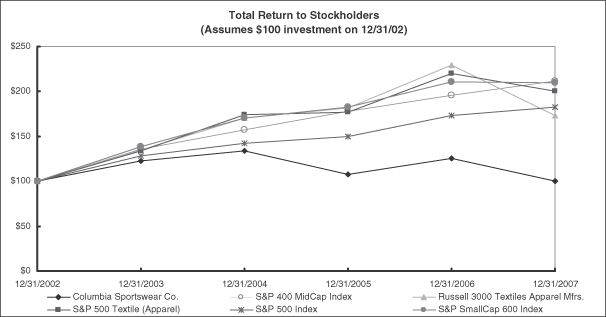

Performance Graph

The line graph below compares the cumulative total shareholder return of our Common Stock with the cumulative total return of the Standard & Poor’s (“S&P”) 400 MidCap Index, S&P 500 Index, S&P Small Cap 600 Index, Russell 3000 Textiles Apparel Manufacturers and the S&P 500 Textile (Apparel) Index for the period beginning December 31, 2002 and ending December 31, 2007. In 2007, we added the S&P 400 MidCap and Russell 3000 Textiles Apparel Manufacturers indices to the performance graph because we believe the companies included in these indices are more comparable to that of Columbia in terms of line of business and market capitalization. The graph assumes that $100 was invested on December 31, 2002, and that any dividends were reinvested.

Historical stock price performance should not be relied on as indicative of future stock price performance.

Columbia Sportswear Company

Stock Price Performance

December 31, 2002—December 31, 2007

| Total Return Analysis |

||||||||||||

| 12/31/2002 | 12/31/2003 | 12/31/2004 | 12/31/2005 | 12/31/2006 | 12/31/2007 | |||||||

| Columbia Sportswear Co. |

$100.00 | $122.69 | $134.20 | $107.45 | $125.69 | $100.48 | ||||||

| S&P 400 MidCap Index |

$100.00 | $135.53 | $157.74 | $177.48 | $195.70 | $211.26 | ||||||

| S&P 500 Index |

$100.00 | $128.63 | $142.59 | $149.58 | $173.01 | $182.39 | ||||||

| S&P SmallCap 600 Index |

$100.00 | $138.73 | $170.08 | $183.02 | $210.62 | $209.95 | ||||||

| Russell 3000 Textiles Apparel Mfrs. |

$100.00 | $134.60 | $170.06 | $181.26 | $229.82 | $172.79 | ||||||

| S&P 500 Textile (Apparel) |

$100.00 | $134.27 | $174.38 | $177.19 | $220.43 | $200.67 |

Securities Authorized for Issuance Under Equity Compensation Plans

See Part III Item 12, Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters, of this Annual Report on Form 10-K for information regarding our securities authorized for issuance under equity compensation plans.

21

| Item 6. | SELECTED FINANCIAL DATA |

Selected Consolidated Financial Data

The selected consolidated financial data presented below for, and as of the end of, each of the years in the five-year period ended December 31, 2007 have been derived from our audited consolidated financial statements. The consolidated financial data should be read in conjunction with the Consolidated Financial Statements and Accompanying Notes that appear elsewhere in this annual report and Management’s Discussion and Analysis of Financial Condition and Results of Operations set forth in Item 7.

| Year Ended December 31, | |||||||||||||||

| 2007 | 2006 (1) | 2005 | 2004 | 2003 | |||||||||||

| (In thousands, except per share amounts) | |||||||||||||||

| Statement of Operations Data: |

|||||||||||||||